Your current location is:{Current column} >>Text

How to Dispute Scam Charges with Your Bank Fast

{Current column}8People have watched

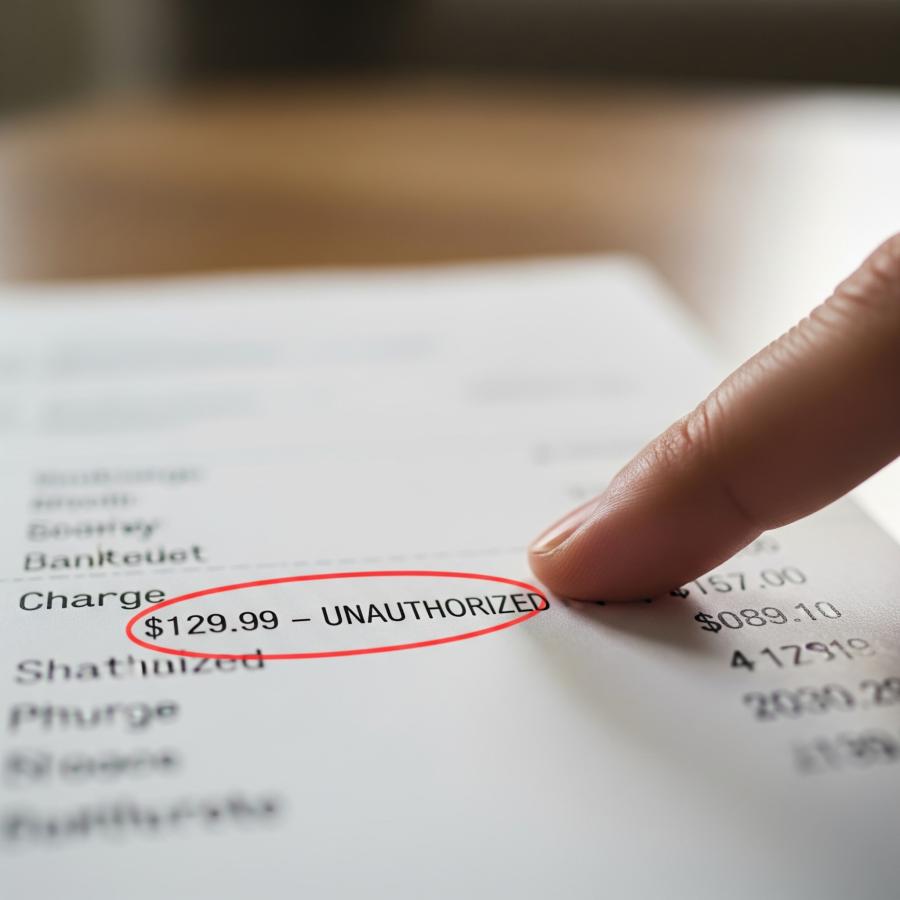

IntroductionSpotted a charge you didn’t make? Here’s what to do next.It shows up on your bank statem ...

Spotted a charge you didn’t make?is fxcm Fuhui Forex legitimate? Here’s what to do next.

It shows up on your bank statement like a bad plot twist.

A charge you didn’t expect. From a company you’ve never heard of.

And suddenly, you’re the main character in a story you didn’t sign up for — the one where your money disappears.

Whether it was a bogus website, a fake seller, or a “free trial” that wasn’t so free, one thing’s clear: you’ve been scammed. Now what?

This isn’t just about chasing refunds. It’s about reclaiming control. In this guide, we’ll show you how to dispute scam charges with your bank — step by step, with tips that actually work. Because getting your money back shouldn’t be a mystery.

Step 1: Confirm It's Actually a Scam

Before you dive into panic mode, take a deep breath and double-check the charge. Some transactions may just look suspicious but aren’t fraudulent. Others? They’re textbook scams.

Could It Be Legit?

Ask yourself:

- Did I forget a subscription renewal?

- Is this a company using a different billing name? (Many apps and services do!)

- Did I sign up for a free trial and forget to cancel?

If the answer to any of these is yes, you may have just made a mistake, not been scammed.

Red Flags for Fraud

But if the charge is:

- Small and random (e.g., $0.99 or $1.17)

- From a company or location you’ve never interacted with

- Repeated in slightly different amounts

- Occurred while your card was physically with you

…it’s probably not legit.

Scammers often test stolen cards by charging a tiny amount first. If that goes through, they may attempt larger transactions.

Don’t ignore it — a small odd charge is often the first sign of something bigger.

Step 2: Act Fast — Contact Your Bank or Credit Card Provider

The moment you suspect fraud, speed is your best defense. The sooner you report it, the better your chances of getting your money back.

Here’s What to Do:

1. Use your bank’s mobile app or websiteto flag the charge.

- Most apps allow you to report suspicious transactions instantly.

2. Call the customer service numberon the back of your card.

- Ask to speak with the fraud department or dispute team.

3. Request a freeze or replacement of your card.

- If your card details are compromised, it’s safest to shut it down completely.

4. Check for other fraudulent transactions.

- If one scam charge slipped through, there may be more, even older ones.

5. Take notes.

- Write down who you spoke with, when, and what they said. You might need this later if the issue escalates.

Why Timing Matters

In many countries, the law protects you, but only if you act fast.

- In the U.S., under the Electronic Fund Transfer Act (EFTA), you must report unauthorized debit card charges within 2 business days to cap your losses at $50.

- Wait more than 60 days? You could lose everything in your account.

- Credit card charges have stronger protections — often “zero liability.”

- In the UK, banks follow the Contingent Reimbursement Model Code, which may offer a full refund, depending on the circumstances.

Step 3: File a Dispute

Once you’ve notified the bank, the next step is to file a formal dispute. This initiates the investigation process.

What You'll Need:

- Your account and transaction details

- Any supporting evidence (e.g., receipts, emails, screenshots of the scam site or messages)

- A written explanation of what happened and why you believe the charge is fraudulent

Most banks let you do this online, but you can also:

- Visit a branch in person

- Call their dispute team

- Send a written letter (especially if requested for documentation)

What Happens Next?

Once your dispute is submitted:

- The bank will typically issue a temporary refund (called a “provisional credit”)

- It may take up to 45 days (or more) for the investigation to be completed

- If the bank agrees it was fraud, the refund becomes permanent

- If they deny your claim, they must explain why, and you can appeal

Keep an eye on your account during this process. If additional charges appear or new scam attempts pop up, notify the bank again.

Step 4: Escalate If the Bank Won’t Help

Most banks want to protect their customers, but not all disputes go your way. If your claim is denied or ignored, don’t give up.

Start by:

- Asking for the official reason your claim was rejected

- Requesting a written report of the findings

- Speaking with a supervisor or submitting a formal complaint within the bank

If you're still stuck, escalate outside the bank:

Where to File a Complaint:

U.S. Residents:

- Consumer Financial Protection Bureau (CFPB): consumerfinance.gov

- Federal Trade Commission (FTC): reportfraud.ftc.gov

- State Attorney General’s Office

UK Residents:

- Financial Ombudsman Service: financial-ombudsman.org.uk

- Action Fraud: actionfraud.police.uk

Canada:

- Canadian Anti-Fraud Centre: antifraudcentre-centreantifraude.ca

- Financial Consumer Agency of Canada

These organizations can often pressure banks to reevaluate or resolve disputes more fairly.

Step 5: Protect Yourself Going Forward

Once you’ve handled the immediate problem, it’s time to fortify your defenses. Scammers may come back for more or try a different angle.

Here’s How to Secure Your Finances:

1. Freeze Your Credit

You can freeze your credit report at no cost from the major credit bureaus. This prevents new accounts from being opened in your name.

2. Set Up Account Alerts

Enable transaction alerts for every charge, even the small ones. Many banks let you set thresholds (like notifications for anything over $1).

3. Use Virtual Cards

Services like Apple Pay, Google Pay, or privacy.com let you generate one-time-use or merchant-specific cards, making it harder for scammers to reuse your info.

4. Secure Your Logins

Use strong, unique passwords and turn on two-factor authentication (2FA)for your banking, email, and shopping accounts.

5. Review Your Statements Regularly

Make it a habit to scan your statements weekly. The earlier you catch something, the better your chances of fixing it.

What If You Got Scammed Outside of a Bank Transaction?

Some scams don’t go through your card or bank directly, like sending money via:

- Wire transfer

- Gift cards

- CashApp, Zelle, or Venmo

- Crypto

These are much harder to recover.

Try This:

1. Contact the payment service immediately

- Some services like Zelle are now offering scam refunds, depending on the case.

2. File a police report

- This creates a paper trail and may help in future claims.

3. Report to scam hotlines or watchdogs

- Many countries have national fraud centers or consumer protection agencies.

4. Warn others

- Leave reviews, report the scam site, or share on scam-tracking platforms like FTI.

Sample Scripts You Can Use

To your bank:

“Hello, I noticed a charge on my account from [Merchant Name] on [Date] for [$Amount]. I did not authorize this and believe it may be fraudulent. I’d like to file a dispute and have my card blocked as a precaution.”

To dispute in writing:

“I am writing to formally dispute a fraudulent charge on my account ending in [XXXX], dated [XX/XX/XXXX] for the amount of [$Amount]. I have never authorized or made a purchase from [Merchant Name]. I have attached supporting documentation, and I request a full investigation and reversal of the charge.”

Bottom Line: It’s Not Your Fault

Getting scammed can feel frustrating and embarrassing, but it happens to millions every year. Scammers are slick, and even the savviest people get caught off guard.

The important thing is not to freeze in fear. Act fast, report the fraud, and take back control. Every step you take helps shut the door on scammers — and keeps your future money safe.

Before you click, check with FTI.com—it’s a quick way to verify websites, phone numbers, crypto wallets, and even IBANs. On mobile? No worries—the FTI app has you covered 24/7, keeping you safer wherever you browse.

Tags:

Related articles

Dollar set for another positive week on raised Fed hike expectations By

{Current column}- The U.S. dollar edged lower in early European trading Friday but was on course for its third conse ...

Read moreHow Will Oil Market Respond to Upcoming Russian Sanctions?

{Current column}I have written in depth about the upcoming Russian oil sanctions and price cap and outlined for how ...

Read moreDollar slips to 5

{Current column}By Samuel IndykLONDON (Reuters) - The dollar was pinned near a five-month low against a basket of ma ...

Read more

Popular Articles

- U.S. crude stocks up 3.69M barrels last week

- Max Power Trading Is Safe? Company Abbreviation Max Power

- Democratic Senator Warnock faces challenge by Trump

- Futures extend losses after robust November jobs report By Reuters

- S&P 500 gives up gains despite Microsoft

- AM Markets Trading Is Safe? Company Abbreviation AM Markets

Latest articles

-

Tesla stock dips as analysts warn price cuts will weigh on margins By

-

Oil rally stalls on weak Chinese data, uncertainty over OPEC cut By

-

Gold slumps below $1,800 as Fed fears resurface By

-

Dollar in retreat; Payrolls release looms large By

-

Stock market today: Dow ends down on Tesla drag, economic jitters By

-

U.S. jobs data, EU Russian oil ban, REIT trouble